Q1 2026 - Constellation Software

Record M&A pipeline (ex. any extraordinarily large deal) during supposed "SaaSpocalypse"

Last Tuesday, Constellation Software (CSI) published its Q1 2026 report and held a conference call with CEO Mark Miller, CFO Jamal Baksh, and CIO Bernie Anzarouth yesterday. The company will also hold its Annual Meeting tomorrow morning (hybrid format), and, amongst other things, talk about some specific AI use cases.

As usual, we’ll go over CSI’s performance including and excluding the spin-out companies, the conference call remarks, the recent M&A news flow, and the updated valuation models. This recap should help you sift through the noise, and focus on the core drivers of forward returns instead. It’s easy to get lost in the headline numbers. At the end of the day, it’s all about reinvesting at high rates of return (and deploying capital frequently), with the market valuing smart capital allocations accordingly over time.

As we stand here today, it’s quite simple - within the VMS space (or any acquisitive software play), CSI (and the whole family for that matter) remains one of the most attractively priced names to own.

Why should we buy say Roper Technologies at a premium when it’s growing EBITA at 6-7% versus CSI’s >15%? High single-digit growth is not competitive enough. The relative valuation argument (“it’s trading at a discount to its own average, so it’s a buy”) does not make sense. It’s an irrelevant discussion for us - we look for attractive (not hyper) growth at a reasonable price.

In a nutshell, CSI’s Q1 results and commentary essentially confirmed what we discussed last March: a solid M&A pipeline with medium and larger-sized deals, as well as typical organic growth. In other words, growing opportunities for capital deployment at healthy IRRs, with Mark Miller’s increased focus on driving organic growth where it makes sense (commensurate with good returns).

Jury’s out on how small VMS business owners will react to seeing public software valuations tank. As Mark Leonard stated last year, during uncertain times, they’re less likely to sell the business they’ve spent their life building. Looking at Topicus’ bread-and-butter type pipeline, there are no signs of a near-term pick-up but CSI has other growth levers to pull.

So far, valuations for small private VMS haven’t budged:

It’s really, at the high end, we could see it maybe plateau a little bit, if not declining slightly in terms of valuations. At the low end where we play, with most of our acquisitions, not at all. - CIO Anzarouth

CSI Standalone

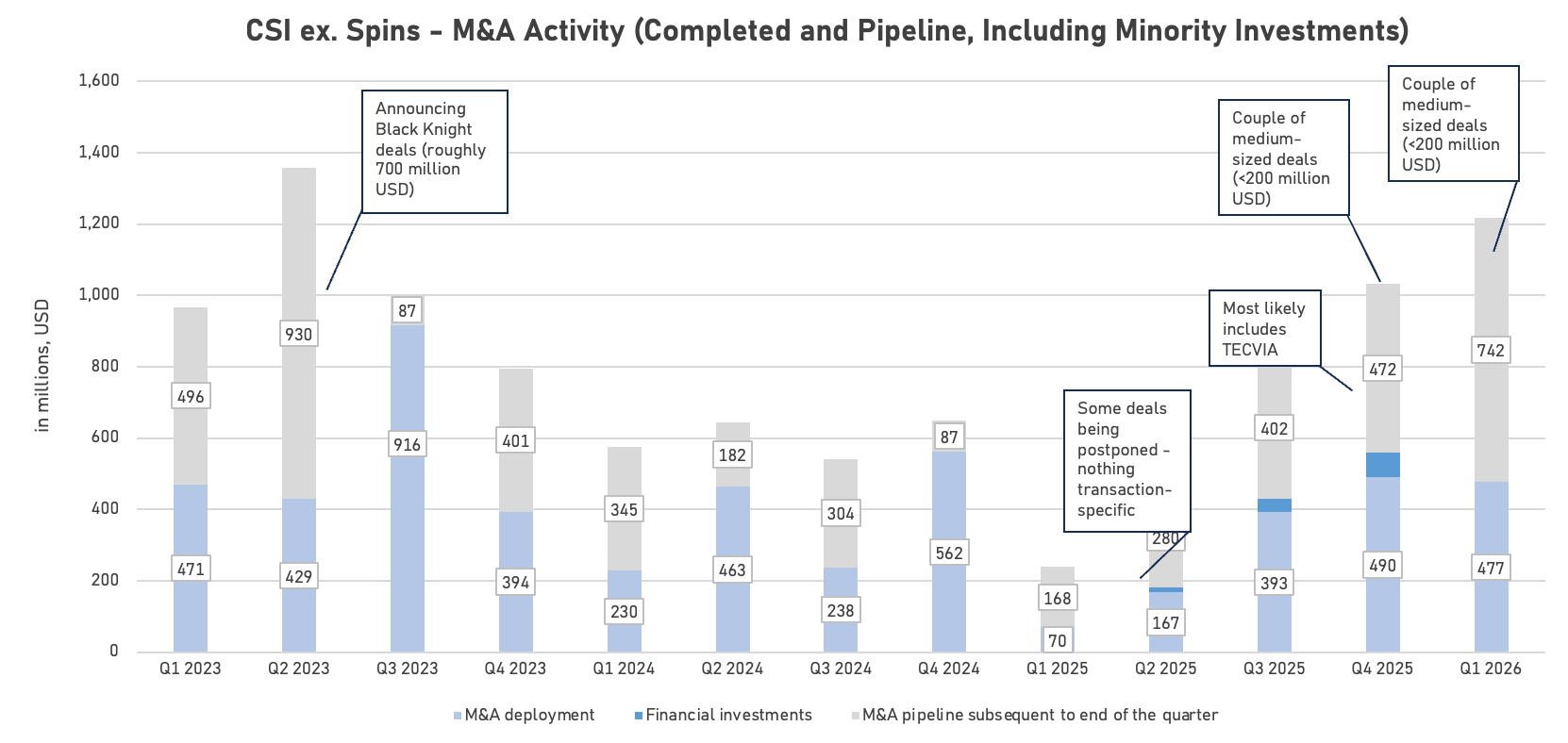

As indicated in the Q4 2025 recap, CSI closed out the year on the strong note with a strong conversion of its M&A pipeline. In Q1, CSI standalone completed deals worth 477 million USD, 5 million USD more than what was indicated in March. Subsequent to the end of Q1, open and/or completed commitments amounted to 742 million USD.

Notes: Prior to Q4 2023, Topicus didn’t disclose the value of its closed deals and/or open commitments. As such, the data for CSI standalone include a portion of Topicus’ M&A pipeline. For Q2 2023, we couldn’t retrieve the info on deals other than the Black Knight transactions. We estimated the remaining M&A pipeline to be worth 230 million USD.

Unsurprisingly, the increased M&A activity (also compared to Q1 2025) comes with some near-term expense pressure and negative mix effects. Nothing worrisome in our view. As Jamal shared:

There were some a couple other acquisitions that were a bit of a drag on margins, like the Q1 cohort of acquisitions themselves were actually a negative margin for the quarter, which, you know, we totally plan to improve them, and it is a typical thing where we improve margins over time.

It was a bit of a bigger drag this quarter than previous quarters. If you look down the like the line items of what’s impacting margins, you can also see hardware margins are slightly down. Again, that’s not 1 of our core products, but again, it was 43% margins versus 46%, and that had about a 20 basis point impact on margins.

Professional services, again, you know, if we’re making acquisitions and using third-party services. On third-party maintenance, you can see that’s up a bit as well, which again, nothing material to call out, but as we use a lot more of these third-party providers and, you know, for coding, et cetera, like you’d expect that to pop up a little bit as well.

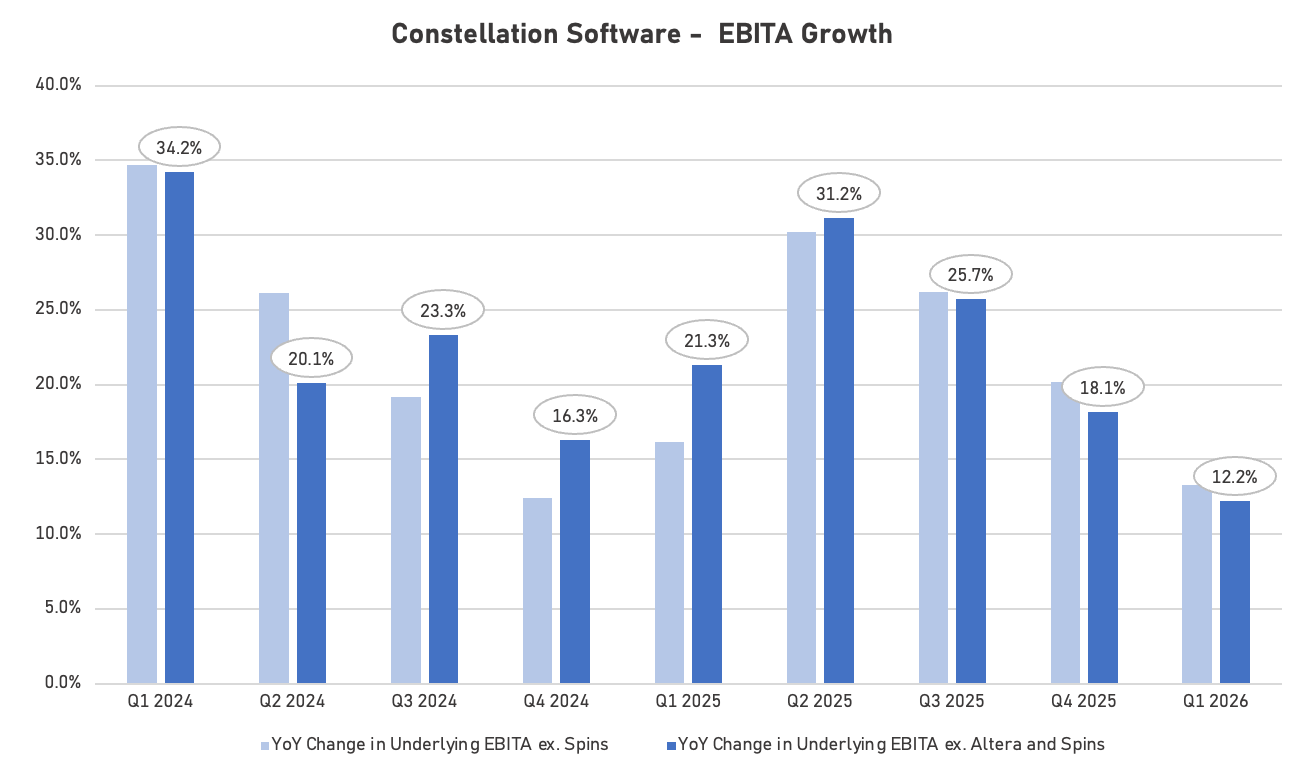

As a result, year-over-year EBITA for CSI grew by “just” 12.2%, excluding earn-out revaluations, the spin-out companies, and Altera (which drove 40% growth against an easy comp but with -6% maintenance revenue growth, resulting in a 19% margin). Excluding FX, growth was about 8%.

The incremental EBITA margin thus came in at 15.6%, the lowest number in a long time. It’s an atypical outcome that’s subject to M&A timing and sizing but one would expect incremental EBITA to rebound over time as we lap today’s higher M&A and integration.

It could be that there will be some higher front-loaded expense pressure as some of CSI’s business units are focused on retooling their organic growth strategy.

I really would like to see them doing a better job on organic growth across the board, and I think this is an opportunity to push them harder on that with the advent of some tools to allow you to do things a little bit faster and a little bit better. - CEO Mark Miller